Rethinking Founder Vesting

The standard vesting schedule for founders in Silicon Valley might be too short. I believe it should be longer.

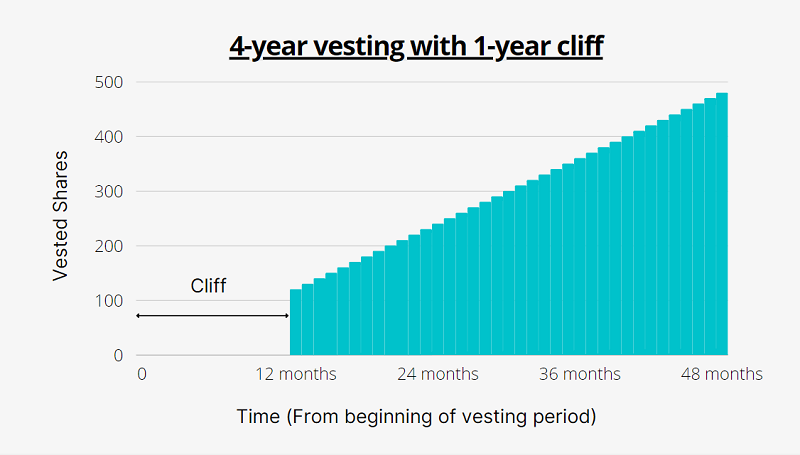

Vesting schedules ensure that equity is earned over time rather than granted upfront. Typically, Silicon Valley founders use a 4-year vesting schedule with a 1-year cliff. This means:

- 1-year cliff: No shares vest during the first year. If you leave before completing one year, you receive nothing.

- After the cliff: 25% of your shares vest at the end of the first year.

- Ongoing vesting: The remaining shares vest gradually over the next three years, usually monthly (1/48 of the total grant).

- Fully vested: After four years, you own 100% of your granted shares.

I’d be curious to know where this standard originated. But regardless of its history, vesting is a necessary practice for companies with multiple founders.

Consider a scenario where one founder leaves after six months, while another stays for four years until the company is sold. It would be unfair for both to receive an equal payout from the sale.

Vesting is a great way to incentivize long-term commitment while protecting the company from early departures. That’s why, when I incorporated my company, I followed this standard too, as Stripe Atlas, an incorporation service widely used for founders here, used this standard as the default term.

The question is whether the vesting term should be “4-year vesting with a 1-year cliff.” Now imagine a company where one founder leaves after four years, while the other works for eight years until it goes public. It would be unfair for both to receive equal payouts from the IPO.

So why don’t we make the vesting period longer? For example, eight years of vesting with a two-year cliff.

There are some concerns with longer vesting.

First, unvested shares at the liquidity event. There is a chance that a company will be sold or go public before the founders’ equity is fully vested. However, this is an easy problem to solve according to our lawyer from Goodwin because you can add an acceleration of vesting clause in your terms; you can make vesting happen faster than otherwise scheduled at liquidity events. On top of that, everything is negotiable in an acquisition. So even your vested shares can be unvested at the point of acquisition.

Second, control. I’ve been discussing the economics of equity, but the other important aspect is control. This may be the biggest risk because you might end up giving your investors more power than you when your vesting takes longer. Investors should have a longer or the same vesting.

Third, investor resistance. Investors may prefer to follow standard terms. If you want to set up different terms from other startups, investors might stay away from your company.

It seems reasonable to have longer vesting as long as founders have enough control over a company and investors are willing to follow the same vesting schedule. That said, I may be missing other concerns, such as potential tax implications.

I’m open to criticism—what do you think?